Enforcement News: SEC Charges Former Executives of High-Performance Glove Manufacturer with Revenue Recognition Fraud

Print Article- Posted on: Apr 15 2020

Regulators and enforcement authorities have often expressed concerns about the revenue recognition practices of corporate entities and those who implement them. Indeed, improper revenue recognition is one of the most common accounting errors pursued by the Securities and Exchange Commission (“SEC” or “Commission”).

To properly recognize revenue, the revenue must be realized and earned. Under generally accepted accounting principles, revenue may be recognized when all the following criteria are met: (1) persuasive evidence of an arrangement exists, (2) delivery of the product has occurred or services have been rendered, (3) the seller’s fee or price is fixed or determinable, and (4) collectibility is reasonably assured. See SEC Staff Accounting Bulletin No. 104, 17 C.F.R. Part 211 (2003) (originally issued in 1999) (here).

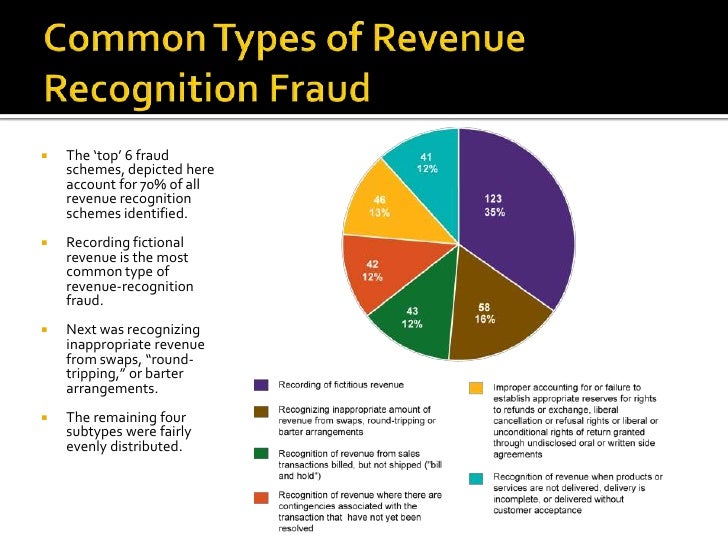

Improper revenue recognition practices come in many shapes and sizes. Some of the more representative forms of improper revenue recognition include: (1) reporting fictitious sales through, among other mechanisms, the use of false sales documents, side agreements, and senior management overrides and adjustments; (2) reporting revenue from “round trip” transactions (i.e., a series of transactions between companies that increase the revenue of the companies involved but, in the end, do not provide any economic benefit to either company), barter arrangements (i.e., the exchange of goods or services between companies) or swaps; (3) “channel stuffing” by using price discounts, extended payment terms or other concessions reflected in undisclosed oral or written side agreements that induce customers to purchase goods they have an unconditional right to return at a later date; (4) “bill and hold” transactions wherein revenue is recognized from a sales transaction that is billed but the goods are not shipped; (5) recognizing revenue for transactions in which there are material contingencies associated with the transaction that are not resolved by the close of the reporting period; and (6) recognizing revenue when the goods or services have not been delivered, or where delivery is not complete, or where delivery has not been accepted by the customer. See Recent Enforcement Actions Involving Revenue Recognition Fraud, PLI Current: The Journal of PLI Press, Vol. 4, No. 1, 2020 (here) (citing Fictitious Revenues, Revenue-Related Financial Statement Fraud (2014-2015 AICPA), slideshare (here), and Understanding Fraud and Our Responsibilities, presented by Jason Lundell (here)).

On April 8, 2020, the SEC announced that it charged three former executives of Ironclad Performance Wear Corp. (“Ironclad”) with fraud for allegedly inflating the company’s revenues through a series of manipulative and deceptive accounting gimmicks. Ironclad’s former Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”) agreed to settle the Commission’s claims.

Based in Farmers Branch, Texas, Ironclad manufactured high-performance gloves for construction, manufacturing, oil, gas, and automotive work. In February 2014, Ironclad hired Jeffrey D. Cordes (“Cordes”) to serve as its CEO. By mid-2014, Cordes brought in William M. Aisenberg (“Aisenberg”) to serve as CFO and Thomas J. Felton (“Felton”) to serve as Senior Vice President of Supply Chain.

According to the SEC’s complaint (here), prior to joining Ironclad, the individual defendants worked together at a private company that sold sporting apparel. Cordes, Aisenberg, and Felton served as Chief Operating Officer, Chief Financial Officer, and Chief Administrative Officer, respectively. That company was acquired and, in August 2014, the acquiring company filed a civil lawsuit against Cordes, Aisenberg, and other associated people and entities, alleging that, among other things, they orchestrated a scheme to inflate the value of certain inventory by staging sham sales and re-purchasing the products at inflated prices. The parties settled the case in 2015.

From at least December 2015 through June 2017 (the “Relevant Period”), alleged the SEC, Cordes, Aisenberg, and Felton falsely inflated Ironclad’s revenues by, among other things, (i) recognizing revenue in the quarter before it was earned and (ii) recognizing revenue that was never earned because the products: (a) were never shipped to, or paid for, by a customer; (b) were exchanged for old products; (c) were cancelled or refused by customers; and/or (d) were never ordered by a customer, including booking nearly $1 million in revenues from a single client for gloves the client never bought, and that Ironclad never shipped. The SEC further alleged that these defendants took affirmative steps to hide their conduct by, among other things, moving products to a warehouse across the street, delaying moving returned product back into inventory, shipping product to different clients, and altering documents, which inflated the quarterly revenues Ironclad publicly reported during the Relevant Period by as much as 24 percent.

The alleged improper revenue recognition was reported to the company by an anonymous source during the second quarter of 2017. In response, Ironclad’s audit committee engaged the company’s outside counsel to review the allegations, and a committee of independent directors later retained an independent law firm to oversee an internal investigation into accounting irregularities.

On July 6, 2017, Ironclad announced in a Form 8-K that investors should no longer rely on the company’s financial statements as of and for the fiscal years ended December 31, 2016 and 2015, and as of fiscal quarters ended March 31, 2017 and March 31, 2016, June 30, 2016, and September 30, 2016. The company also announced that Cordes and Aisenberg resigned from their positions with the company. Felton was terminated the following week by Ironclad’s new management.

On September 8, 2017, Ironclad and Ironclad Performance Wear Corp. California (“ICPW California”), a wholly owned subsidiary of Ironclad and the entity through which all Ironclad-related operations were conducted, filed voluntary petitions for relief under Chapter 11 of the Bankruptcy Code. Later that month, Ironclad’s auditor resigned effective September 22, 2017, noting material weaknesses in Ironclad’s tone at the top, entity-level controls, and revenue recognition.

On November 14, 2017, Ironclad and ICPW California completed a sale of substantially all of their assets. The companies also filed a plan of liquidation, which was approved by the United States Bankruptcy Court for the Central District of California and became effective on February 28, 2018.

The SEC filed its complaint in the U.S. District Court for the Northern District of Texas. The Commission alleged that Cordes, Aisenberg, and Felton violated the antifraud provisions of Sections 17(a)(1) and (3) of the Securities Act of 1933 (“Securities Act”) and Section 10(b) of the Securities Exchange Act of 1934 (“Exchange Act”) and Rules 10b-5(a) and 10b-5(c) promulgated thereunder, or in the alternative that Felton aided and abetted these violations by Cordes and Aisenberg. The complaint further alleged that Cordes and Aisenberg violated Section 10(b) of the Exchange Act and Rule 10b-5(b) thereunder. The complaint also charged Cordes, Aisenberg, and Felton with violating the reporting, books and records, and internal accounting control provisions of Sections 13(a), 13(b)(2)(A), and 13(b)(5) of the Exchange Act and Rules 12b-20, 13a-1, 13a-11, 13a-13, 13b2-1, and 13b2-2 thereunder, and Cordes and Aisenberg with violating Section 13(b)(2)(B) of the Exchange Act and Rule 13a-14 thereunder.

Without admitting or denying the allegations, Cordes and Aisenberg consented to the entry of final judgments that imposed permanent injunctions and officer and director bars and required each to pay a $173,437 civil penalty. The settlements are subject to court approval. The SEC’s litigation against Felton remains ongoing.

See Lit. Rel. No. 24792 (April 8, 2020) (here).

{kind=link}